Executive Summary. The Trump Administration’s bold economic and job creation vision (i.e., sustained 4% GDP growth and 25 million new jobs) is progressing as planned albeit with some bumps in the road. As addressed in this analysis, recent employment and economic reports present a positive but mixed picture on President Trump’s progress during his first 10-months in office.

On the bright side, 261,000 new jobs were created. 250,000 new jobs per month is the standard accepted by most economists to compensate for downturns and sustain robust economic growth. This standard has been exceeded only 30-times during the 202-months since the turn of the Century. In addition, for the second month in a row, U.S. GDP growth was at or slightly above 3.0%, the unemployment rate dropped to a new post-recession low of 4.1% freeing more 281,000 Americans from the bondage of unemployment, and the Administration maintained the run of 85-months of consecutive labor force gains.

On the negative side of the economic and labor force ledger, the number of sidelined citizens categorized as “not-in-the-labor-force” increased by 968,000 people—the largest number of voluntary workforce departures since January 2012. Also on the negative side of the ledger, small businesses continue to struggle, but Jobenomics is hopeful that the recently announced Congressional Tax Cuts and Jobs Act will stimulate startup and small business growth via the reduction of the corporate tax rate on 28 million incorporated and unincorporated small businesses.

Download complete report: Jobenomics Employment & GDP Report, 3 November 2017

Jobenomics Historical Employment and GDP Analysis. The question that policy-makers, pundits and the general public really want to know is how does the latest job creation number compare to past history?

Jobs Gains/Losses Since 2001

As shown, since 2001, the monthly job creation high water mark of 524,000 new jobs was achieved in May 2010, and the low water mark for jobs losses was 823,000 in March 2009. From an Administration standpoint,

- The Bush Administration (2001 to 2008) created an average of only 22,000 new jobs per month, due to the onslaught of two major recessions, the calamity of 9/11 and the United States’ expensive mobilization for the global war on terrorism.

- The Obama Administration (2009 to 2016) created an average 109,000 job gains per month. If the six months of the Great Recession that Obama “inherited” was subtracted, the average of the ensuing 90-month period yielded an average of 159,000 new jobs per month. Perhaps, the greatest legacy of the Obama Administration is 75-months of consecutive job gains averaging 199,000 jobs per month (not shown) during a period where the U.S. economy grew at a sclerotic rate of only 1.5%.

- The Trump Administration continued the positive job creation trend with 10 consecutive months of job gains and extended the continuous job creation run to 85 months—the longest span of labor force gains since the Bureau of Labor Statistics began record keeping in February 1939. To date, the Trump Administration is averaging 169,000 job gains per month, which is good but insufficient for the Trump Administrations to create 25 million new jobs over the next decade. Jobenomics asserts that the overall economy and labor force is gaining momentum and is likely to accelerate into high-gear when Washington revamps the tax code.

To achieve President Trump’s goal of creating 25 million new jobs over the next ten years, the Administration needs to generate 211,955 new jobs per month. To compensate for good and bad months, 250,000 jobs per month is a reasonable standard that is accepted by most economists to compensate for workforce downturns and create a workforce that will produce enough goods and services to grow GDP. During the recent 85-month run of job gains, the 250,000 job gain standard was exceeded 20-times, or nearly one out of every four months. So, increasing the job creation threshold to 250,000 is an achievable goal, especially if more attention is proffered to small business creation.

Small business is unquestionably the engine of the U.S. economy. 28 million U.S. small businesses employ the majority of all Americans and created the majority of all new U.S. jobs this decade. On 2 November 2017, the Republican-controlled U.S. House of Representatives released their version of the “Tax Cuts and Jobs Act” that chops the corporate tax rate from 35% to 20% on incorporated small business and reduces the tax rate form 39.6% to 25% for unincorporated “pass through” businesses (sole proprietorships, partnerships, and S-Corporations that pay taxes based the owner’s personal income tax returns). If each of these 28 million small businesses hired only one (1) net new employee over the next several years, Trump’s 25 million new jobs goal could be realized in a much shorter time frame than currently envisioned.

From a Jobenomics standpoint, job gain/loss statistics are important, but they are only a prelude to a much more important question regarding net labor force gains and losses. As will be discussed in detail in this report, the U.S. labor force consists of 255,562,000 citizens (called the civilian noninstitutional population) who are working, unemployed, and able-bodied adults who can work but choose not to work for a multiplicity of reasons.

To fully understand net labor force gains and losses, Jobenomics uses two primary sources of U.S. labor force data: (1) the monthly U.S. Bureau of Labor Statistics (BLS) Employment Situation Summary, a monthly summary of all U.S. government and private sector employment, and (2) the ADP National Employment Report, a monthly survey of employment by 400,000 U.S. private sector businesses by the ADP Research Institute in collaboration with Moody’s Analytics.

Jobenomics Analysis of the BLS Employment Situation Summary Report.

BLS Employment Situation Summary, 3 November 2017

On 3 November 2017, the BLS reported that October’s total nonfarm payroll employment increased by 261,000 and revised September’s estimate from a loss of 33,000 jobs to a gain of 18,000, which maintained the 85 months of consecutive labor force gains—the longest span of labor force gains since BLS record keeping began in February 1939. The BLS also reported that the U3 unemployment rate dropped to a new post-recession low of 4.1% freeing an additional 281,000 Americans from the bondage of unemployment. On the opposite side of the labor force ledger, 968,000 more citizens, categorized as “not-in-the-labor-force”, voluntarily departed the U.S. labor force for a variety of reasons including welfare, early retirement and education. These voluntary workforce departures of capable adult citizens mitigated the otherwise good news of the overall U.S. employment situation causing a net loss of 426,000 workers as highlighted above in light green.

The October BLS report included only some of the severe economic and workforce impacts of Hurricanes Harvey, Irma, and Maria (and to a minimum degree Hurricane Nate) and is the likely reason for the high number of workforce departures. The economic impact of these storms is estimated in to be as high as $300 billion due to property damage, lost output, insurance claims and federal aid. Labor force shocks are also likely to be recorded in subsequent employment reports. Hurricane Katrina sidelined an estimated 800,000 employees and Hurricane Sandy sidelined 400,000 workers and caused many small businesses to close. The economic impact of Harvey, Irma and Maria are likely to be more onerous than Katrina and Sandy.

- Total employment of Houston, South Western Florida and Puerto Rico is approximately 7 million workers. While there are no official assessments of sidelined workers in these afflicted areas, it is reasonable to estimate that several million workers were, and will continue to be, sidelined. Almost the entire workforce of 1 million Puerto Ricans were paralyzed due to power outages and destruction of much of the island’s aging infrastructure. Moody’ Analytics, a leading risk management and research firm, predicts that recovery operations from recent storms will take 6-months to recover 80% of the economy and up to 3-years to reach 100%.[1]

- Unfortunately, the United States is still in the early phases of disaster recovery from the hurricane trifecta. Five phases of disaster recovery include search and rescue, emergency relief, early recovery, mid to long term recovery, and community development. Construction, durable goods (e.g., automotive, household appliances and home furnishings), non-durable goods (e.g., food, clothing and commodities) and professional services should be the first business sectors to rebound from the calamity due to tens of billions of dollars of disaster recovery spending. However, tens of thousands of retail operations and underinsured homeowners and small business are likely to remain shuttered for quite a while, or forever.

- Given the massive economic scope of these disasters, there may not be enough federal money to fund needed recovery operations let alone for community and infrastructure development for communities like Puerto Rico that is in $70 billion debt.

The October BLS report also provides a strategic perspective on the state of the U.S. labor force that underpins the entire U.S. economy.

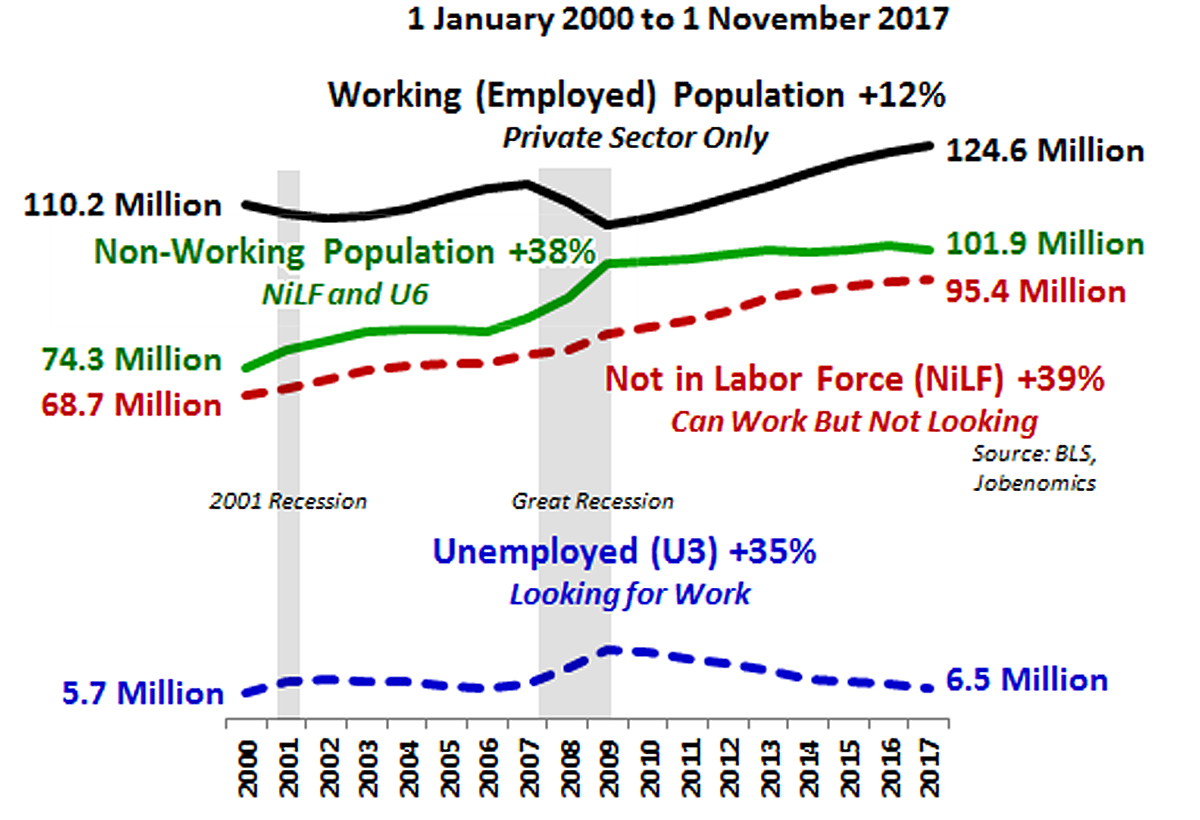

Working Versus Non-Working Populations

This graph presents a strategic perspective of the U.S. private sector workforce covering the time period from 1 January 2000 to 1 November 2017. The private sector produces the vast majority of goods and services that drives economic growth. Since the turn of the 21st Century, the U.S. private sector’s Working (Employed) population rose by 12% compared to a rise of 38% in the Non-Working Population. Jobenomics defines the Non-Working Population as Not-in-Labor Force (that rose by 39%) and the Officially U3 Unemployed (which is still 35% higher today than in year 2000 in terms of numbers of unemployed). It is important to notice on the above chart, that the Non-Working Population almost equaled the size of the Working Population at the end of the Great Recession. Since the Great Recession the Working Population has grown while the Non-Working Population has stabilized. The question to ponder for the future is whether employment and economic (GDP) growth can continue to grow the workforce while simultaneously reducing the Not-in-Labor cadre substantially.

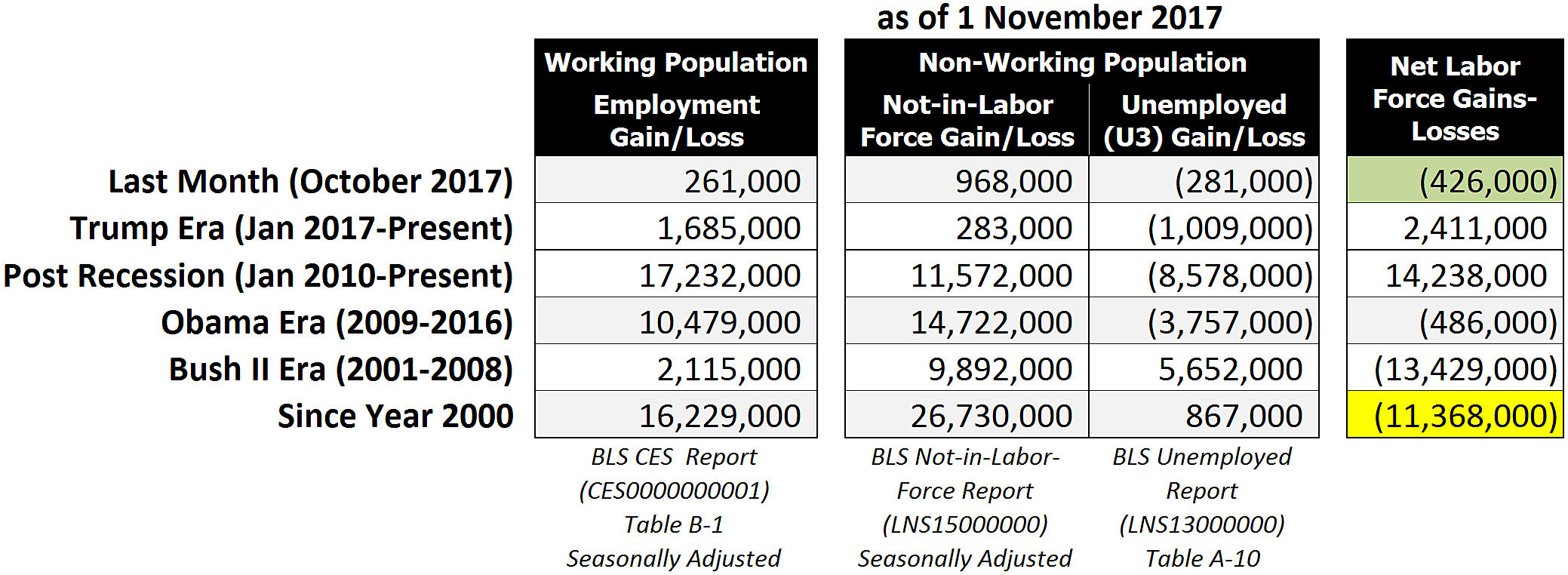

U.S. Labor Force Gains and Losses Since 2000

In October 2017, the Working Population (private sector employment) increased by 261,000 jobs and the Non-Working Population degraded with 968,000 more people enrolled in the Not-in-Labor-Force (a BLS category of for people who can work but choose not to work) and 280,000 fewer unemployed citizens. The BLS also reported that the Official U3 Unemployment rate dropped from 4.2% to 4.1% a post-recession low. From a historical unemployment rate perspective, the post-WWII low was 2.5% in June 1953, followed by 3.4% in May 1969 and 3.8% in April 2000. As highlighted in green, the net labor force loss in October was 426,000.

During the 10-months of the Trump Administration, Working Population gains amounted to 1,685,000 workers, for an average of 168,500 per month, which is below the desired threshold of 250,000 jobs per month. However, the Not-in-Labor-Force and U3 Unemployment categories recorded positive reductions of 283,000 and 1,009,000 respectively. The Trump Administration net labor force gain equates to 2,411,000 over the first 10-months of President Trump’s first term in office. This 10-month net gain of 2,747,000 compares very favorably with the Obama Administration’s 8-year/96-month labor force net loss of 486,000 workers and the GW Bush Administration’s 8-year/96-month devastating workforce net loss of 13,429,000. While positive, it is too early to foretell if the Trump Administration’s favorable statistics will stand up to the test of time compared to the economic and workforce calamities that challenged former Administrations.

Since the end of the Great Recession, from 1 January 2010 to 1 November 2017, the U.S. labor force net gain was 14,238,000 workers. 17,232,000 new workers entered the labor force. 8,578,000 workers departed unemployment rolls. Unfortunately, a corresponding number of citizens joined the ranks of the Not-in-Labor-Force that rose by 11,572,000 citizens.

During the 8-years of the Obama Era (1 January 2009 through 31 December 2016), the U.S. labor force lost a net 486,000 jobs, with 10,479,000 entering the labor force, 14,722,000 voluntarily departing, and 3,757,000 fewer people recorded as officially unemployed. It is important to remember that the first 21-months of President Obama’s first term in office, the Administration dealt with the Great Recession and recovery operations. Obama’s next 75-months in office produced the longest run of consecutive labor gains since WWII when BLS record keeping began. This 75-month run greatly exceeded the previous record of 48-months that occurred in the July 1986 to June 1990.

During the 8-years/96-months of the Bush II Era (1 January 2001 through 31 December 2008), the U.S. labor force lost a net 13,429,000 jobs, which included the 8-months of the 2001 Recession (March 2001 through November 2001) and 13-months of Great Recession (December 2007 through December 2008), the aftermath of the September 11, 2001 attacks, the ensuing global war on terrorism as well as Hurricanes Katrina, Ike, Rita, Wilma, Ivan, Charley, Frances, Jeanne and Allison that collectively caused over $275 billion in damage. As a result of these constant calamities, all three labor force sectors yielded negative results: only 2,115,000 workers entered the labor force (an abysmal average of only 22,000 new jobs per month), 9,892,000 able-bodied citizens voluntarily departed, and 5,652,000 people were added to the unemployment rolls.

From the beginning of the 21st Century (1 January 2000 to 1 November 2017), the American labor force is still weaker by a net 11,368,000 workers (highlighted in yellow). This weakness is exacerbated by a population growth of 44 million additional American citizens present today compared to 2000 (282 million versus 326 million) plus the impact of a rapid rise of contingent part-time workers with a commensurate decrease in traditional full-time workers.

To sum up, BLS data indicates that the U.S. economy cannot be sustained without strengthening of the U.S. private sector’s labor force. The private sector workforce consists of 124,322,000 workers, which represents only 38% of the total U.S. population of 326 million. Of the private sector workforce, approximately 60% are traditional full-time workers and 40% are contingent workers (part-timers, freelancers, independent contractors, etc.) who earn far less income than traditional workers and often receive little or no benefits. To achieve economic and labor force growth, policy-makers and decision-leaders must concentrate on small business creation and sustainment.

Jobenomics Analysis of the ADP National Employment Report.

The October 2017 ADP National Employment Report, released on 1 November 2017, states that the U.S. non-farm private sector created 235,000 new jobs, which is slightly less than the 252,000 new private sector jobs reported by the BLS.[2] Note: preliminary BLS Employment Situation Summary estimates of 252,000 new non-farm private sector jobs and 9,000 government new employees for a total of 261,000 jobs. ADP does not report on government employment, unemployment or workforce departures as does the BLS.

Of the 235,000 U.S. non-farm private sector new jobs, small businesses (1-49 employees) gained 79,000 jobs, medium businesses (50-499 employees) gained 66,000 new jobs, and large businesses (500+ employees) gained 90,000 new jobs. Service-providing industries created 190,000 with Professional/Business Services and Health Care/Social Assistance services being the star performers producing 51,000 and 44,000 new jobs respectively. Goods-producing industries created 48,000 jobs with Construction and Manufacturing producing 29,000 and 18,000 jobs respectively. The biggest losers were the Trade/Transportation/Utilities, Non-Internet Information and Education sectors with losses of 50,000, 27,000 and 5,000 employees.

For the purposes of this report, Jobenomics classifies small business as having 1-499 employees (the definition supported by the U.S. Small Business Administration), midsized business as 500-999 and large businesses as 1000+ employees. In addition, Jobenomics defines micro-businesses as having 1-19 employees that includes self-employed firms.

U.S. Private Sector Employment by Company Size

As reported by ADP, small businesses are undeniably the dominant employer in the United States. Small businesses with less than 500 employees employ 77.1% of all private sector Americans with a total of 96,501,492 employees—over 3.4-times the amount of large businesses with more than 500 employees that have 28,622,035 employees. Micro-businesses with 1-19 employees employ 1.6-times the number of major corporations with over 1,000 employees (31,332,986 versus 20,080,195).

U.S. Private Sector Jobs Created This Decade by Company Size

Since the beginning of this decade, small businesses created 72.6% of all new jobs in the United States. Small businesses with less than 500 employees created 2.6-times more jobs as large businesses with 500+ employees, or 13,075,803 versus 4,936,551 new jobs respectively. Micro and self-employed businesses with 1-19 employees created 82% as many jobs as major corporations with over 1,000 employees (3,045,157 versus 3,709,984).

U.S. Private Sector Jobs Created Last Month by Company Size

Last month (October 2017), U.S. small business (1-499 employees) created 61.9% of all new jobs compared to 41.9% in September, 51.7% in August, 74.6% in July, 68.4% in June, 77.2% in May, 72.2% in April and 81.9% in March.

U.S. Micro-Business Job Creation Engine Is Faltering

Alarmingly, micro-business job creation has dropped by almost 60% since the post-recession peak in April 2011. Micro-businesses underpin the U.S. economy. Continued denigration of these businesses can only led to economic stagnation.

Of the 4 million micro-businesses created over the last decade, tens of thousands of ultra-high growth businesses (called unicorns and gazelles) have generated millions of net new jobs for America. According to the Kauffman Foundation, these fleet-footed startups account for 50% of all new jobs created. Uber, Lyft, Airbnb, SpaceX, WeWork and Pinterest are recent examples of unicorns—a startup company that rapidly achieves a stock market evaluation of $1 billion or more. A gazelle is high-growth company (of any size, but usually a recent entrepreneurial startup or micro-business) that increase revenues by over 20% per year for over four years or more.[3] The top-10 U.S. gazelles include Natural Health Trends, Paycom Software, Lending Tree, ABIOMED, MiMedx Group, Facebook, NetEase, Ellie Mae, Amazon.com and Arista Networks, according to Fortune magazine.[4]

Micro-businesses are the life blood of the emerging digital economy that will equal the size and scope of today’s traditional economy within the next few decades. If America fails to compete effectively in the global digital economy, it will quickly be relegated to a back-bench position to countries like China. China has a much superior digital economy strategy and a public/private implementation effort than the United States. For information on this topic, download the Jobenomics’ “China’s Digital Economy Quest” report at https://jobenomicsblog.com/chinas-digital-economy-quest/.

Jobenomics Analysis of Various Economic Reports.

The rate of small business startups is also dropping precipitously. Business startups are the seed corn of the U.S. economy. Without the planting and fertilization of these seedlings the fields of American commerce will be fallow.

In terms of new starts (firms less than 1-year old), the Census Bureau’s Business Dynamic Statistics (BDS) indicate that the United States is now creating startup businesses at historically low rates, down from 16.5% of all firms to 8% in 2014 (latest data).[5] Based on a Wall Street Journal (WSJ) analysis of this Census Bureau data, “If the U.S. were creating new firms at the same rate as in the 1980s…more than 200,000 companies and 1.8 million jobs a year” would have been created.[6]

During the heydays of the 1970s, Bill Gates and Steve Jobs started Microsoft and Apple, two of the largest U.S. companies today with market capitalization of $890 billion and $650 billion respectively as of 1 November 2017. One has to wonder, if these companies would have been launched in our current austere startup environment and the lack of attention of current Washington policy-makers?

According to a Census Bureau’s BDS press release on 20 September 2017, in 2015, 414,000 U.S. startup firms created 2.5 million new jobs, which is well below the pre-Great Recession average of 524,000 startup firms and 3.3 million new jobs per year for the period 2002-2006.[7] In 2015, job creation minus job destruction equaled net job creation of 3.1 million, which supports the Jobenomics hypothesis that net job creation is a far more important statistic for policy-makers than just focusing on only new jobs. Other tidbits of the 2017 BDS press release include:

- In 2015, 5 million U.S. small businesses (1-499 employees) created 45% (1,400,711) of all net new jobs compared to 20 thousand large businesses (500+ employees) who created 55% (1,690,591) net new jobs.

- In 2015, 4.5 million micro-businesses (1-19 employees) net job creation equated to 14% (434,203) of all net new jobs. Most of these jobs were produced at the base of America’s socioeconomic pyramid, a demographic that receives little attention from big business. If U.S. policy-makers paid more attention to startup and micro-business job creation, the U.S. labor force and economy would be far more robust than it is today.

- In 2015, net job creation in urban areas was over twice the rate of rural areas, or 2.7% versus 1.2% respectively. This supports Jobenomics assertion that urban renewal, with emphasis on blighted inner-city communities, will not only create the maximum number of new jobs but will also produce positive collateral benefits of poverty and crime reduction.

According to another Kauffman Foundation analysis of the Census Bureau’s Business Dynamic Statistics, most city and state government policies that look to big business for job creation are doomed to failure because they are based on unrealistic employment growth models. “It’s not just net job creation that startups dominate. While older firms lose more jobs than they create, those gross flows decline as firm’s age. On average, one-year-old firms create nearly 1,000,000 jobs, while ten-year-old firms generate 300,000. The notion that firms bulk up as they age is, in the aggregate, not supported by data.”[8]

Jobenomics agrees with both the WSJ and Kauffman analyses. Moreover, the Jobenomics 20-part series, entitled President Trump’s New Economy Challenge (which is posted on the Jobenomics.com website from 6 February 2017 to 10 April 2017) provides a detailed analysis why the Trump Administration’s bold economic (4% GDP) and job creation (25 million new jobs) vision is likely to fall short due to its concentration on big business rather than small business creation and sustainment.

Not only is small business critical to net job creation, it is the primary determinant for GDP growth given the fact that big businesses are increasingly looking at automation and outsourcing (to foreign workers or domestic contingency workers) to replace the standard full-time labor force.

The ideal rate for U.S. GDP growth is around 3%. Any GDP growth below 2% is considered sclerotic growth that makes the U.S. economy vulnerable to financial downturns.

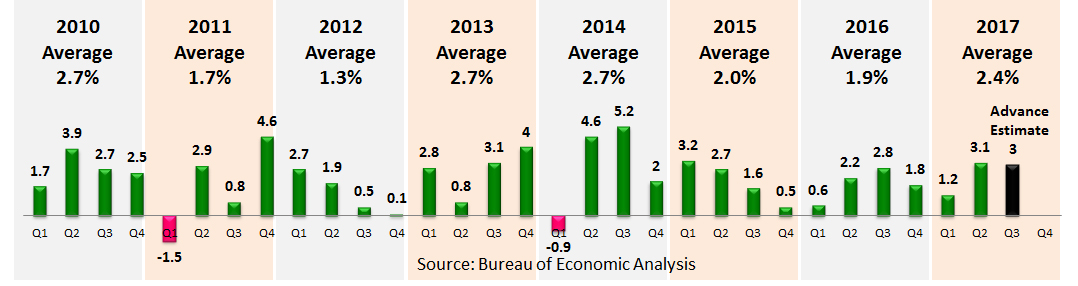

Real GDP Quarterly Percent Change This Decade

According to the U.S. Bureau of Economic Analysis (BEA), during the post-recession recovery period from Q1 2010 through Q2 2017, U.S. GDP averaged 2.3%. In 2015 and 2016, U.S. GDP grew by subpar rates of 2.0% and 1.9% respectively. During the first three quarters of the Trump Administration, GDP averaged 2.4%. However, the last two quarters have posted 3.1% and 3.0% (advance estimate) gains.[9]

Q1 2017 (January, February and March 2017)’s GDP final estimate was a subpar 1.2%—up from an abysmal “advance” estimate of 0.7%, equal to the 1.2% “second” estimate, and down from the 1.4% “third” estimate. Regardless of estimate, Q1 GDP data was not good news for the new Trump Administration. However, these low percentages can be rationalized as a carryover from the previous Administration.

Q2 2017 (April, May and June 2017)’s GDP is 3.1%, up from an “advance” estimate of 2.6%—a significant improvement over Q1 and a good sign for President Trump’s stated goal of raising U.S. GDP growth to 4.0%.[10]

The BEA’s advance estimate for Q3 2017 (July, August and September 2017) is 3.0%. However, there are a number of other highly credible prognosticators that are making Q3 2017 forecasts. The Federal Reserve Bank of Atlanta’s GDPNow forecast model for Q3 2017 is 2.5% as of 26 October 2017. The “Blue Chip” survey of the bottom 10 and top 10 leading business economists forecast that Q3 2017 growth will eventually fall between 1.7% and 2.9%.[11]

For Q4 2017, the Federal Reserve Bank of Atlanta’s GDPNow forecast is 3.3% as of 3 November 2017, up from 2.9 on 30 October 2017. The “Blue Chip” survey of the bottom 10 and top 10 leading business economists forecast that Q3 2017 growth will eventually fall between 2.1% and 3.2%.[12]

While GDP growth does not insure employment growth, sclerotic GDP growth discourages business hiring, consumer spending and labor force expansion. Sclerotic GDP growth also discourages lower rates of unemployment and voluntary workforce departures. Negative GDP growth creates recessions and depressions depending on the severity and longevity of the contracting economy.

The period of sclerotic GDP growth from 2000, has dramatically impacted the American middle-class and the U.S. labor force that is weaker by 11 million workers today than at the beginning of the 21st Century. Even though wages have improved in the last year, for most American workers, real wages (purchasing power) have not increased significantly for decades. America’s aggregate household income has shifted from middle-income to upper-income households, causing many middle-class workers to leave the workforce altogether. The solution to building a robust middle-class is to accelerate GDP growth, which requires the creation of more productive private sector jobs, which, in turn, can only be generated by a massive expansion of the small business sector.

Concluding Thoughts.

President Trump’s vision of a “dynamic and booming economy” is one that can produce a GDP growth rate of “4% over the next decade”. This vision ultimately depends on mass-producing business, especially small business, in sufficient quantities to create 25 million net new jobs. Sclerotic (0% to 2%) or recessive (negative) GDP rates depreciate a government’s legitimacy. Robust GDP growth of over 3% will have the opposite effect.

According to the nonpartisan Congressional Budget Office’s 2017 to 2027 Budget and Economic Outlook report[13], “over the next five years, the monthly increase in nonfarm payroll employment, which is estimated to average 160,000 jobs in the first half of 2017, is projected to settle down to an average of 64,000 jobs.” If this CBO forecast is correct, the next decade is likely to produce only 9 million American jobs, which is far short of President Trump’s projection of 25 million new jobs. Note: last year’s BLS Employment Projections: 2014-24 Summary report[14] forecasts that the United States will produce only 9.9 million new jobs over the next decade.

Jobenomics tends to agree with these gloomy CBO and BLS forecasts for the reasons discussed in the Jobenomics 20-part series entitled President Trumps New Economy Challenge.[15] However, the Trump Plan can be amended to change CBO and BLS labor force projections from negative to positive.

With proper leadership, the Administration can lift tens of millions of Americans out of poverty by making the following four structural changes to President Trump’s economic and job creation plan:

- Balancing the traditional standard industrial economy with the newly emerging nonstandard digital economy,

- Mitigating the mass-exodus of able-bodied workers who are voluntarily departing the U.S. labor force for lives of dependency and alternative (often illicit) lifestyles,

- Addressing the challenge of the ever-growing contingency workforce that will soon be the dominate form of labor in the United States, and

- Mass-producing small and self-employed businesses—the engine of the U.S. economy—and the employer of the vast majority of Americans.

If the Trump Administration can achieve 4% GDP growth in a stable global economy, the U.S. economy will boom and Americans will be euphoric. This feat will not be easy. The last year the United States reached 4% in a single year was 2001. The last time that the United State reached 4% in ten consecutive years during the last 50-years was never (3.5% was the highest from 1976 to 1985). Notwithstanding, if the Trump Administration can tie the 3.5% record over the next decade, they will be vindicated and worthy of much praise.

About Jobenomics: Jobenomics deals with economics of business and job creation. The non-partisan Jobenomics National Grassroots Movement’s goal is to facilitate an environment that will create 20 million net new middle-class U.S. jobs within a decade. The Movement has a following of an estimated 20 million people. The Jobenomics website contains numerous books and material on how to mass-produce small business and jobs as well as valuable material on economic and business trends. For more information see https://jobenomics.com/.

[1] Fortune, The Hidden Costs of Hurricanes, 22 September 2017, http://fortune.com/2017/09/22/hurricane-maria-irma-harvey-damage-cost/

[2] ADP National Employment Report, Press Release, 4 October 2017, http://www.adpemploymentreport.com/2017/September/NER/docs/ADP-NATIONAL-EMPLOYMENT-REPORT-September2017-Final-Press-Release.pdf

[3] Kauffman Foundation, The Economic Impact Of High-Growth Startups, 7 June 2016, http://www.kauffman.org/newsroom/2016/06/understanding-the-economic

[4] Fortune, 100 Fastest Growing Companies, The Top 10, 2017, http://fortune.com/100-fastest-growing-companies/list/

[5] U.S. Census Bureau, Business Dynamics Statistics, Firm Characteristics Data Tables (1977-2014), Firm Age, retrieved 4 October 2017, https://www.census.gov/ces/dataproducts/bds/data_firm.html

[6] Wall Street Journal, Sputtering Startups Weigh on U.S. Economic Growth, 23 October 2016, http://www.wsj.com/articles/sputtering-startups-weigh-on-u-s-economic-growth-1477235874?mod=djem10point

[7] U.S. Census Bureau, Business Dynamics Statistics, Newsroom, 20 September 2017, Startup Firms Created Over 2 Million Jobs in 2015, https://www.census.gov/newsroom/press-releases/2017/business-dynamics.html

[8] Kauffman Foundation, The Importance of Startups in Job Creation and Job Destruction, Last Paragraph, 9 Sep 2010, http://www.kauffman.org/what-we-do/research/firm-formation-and-growth-series/the-importance-of-startups-in-job-creation-and-job-destruction

[9] U.S. Bureau of Economic Analysis, Table 1.1.1 Percent Change From Preceding Period in Real Gross Domestic Product, https://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm

[10] White House Website, https://www.whitehouse.gov/bringing-back-jobs-and-growth

[11] The Federal Reserve Bank of Atlanta’s, GDPNow, https://www.frbatlanta.org/cqer/research/gdpnow.aspx

[12] The Federal Reserve Bank of Atlanta’s, GDPNow, https://www.frbatlanta.org/cqer/research/gdpnow.aspx

[13] Congressional Budget Office, Budget and Economic Outlook: 2017 to 2027, January 2017, https://www.cbo.gov/sites/default/files/52370-Outlook_OneColumn.pdf

[14] BLS Employment Projections 2014-2024 Report, https://www.bls.gov/news.release/ecopro.toc.htm

[15] Jobenomics, https://jobenomicsblog.com/president-trumps-new-economy-challenge/